Ron Legrand – Private Lending

$95.00$997.00 (-90%)

Getting money to do real estate deals has nothing to do with going to a bank, filling out an application, putting up down payments or waiting to be approved. Smart investors won’t go near banks who want to control their lives and tell them what they can or can’t qualify to borrow.

Author: Ron Legrand

Ron Legrand – Private Lending

Check it out: Ron Legrand – Private Lending

Getting money to do real estate deals has nothing to do with going to a bank, filling out an application, putting up down payments or waiting to be approved. Smart investors won’t go near banks who want to control their lives and tell them what they can or can’t qualify to borrow.

When I started in 1982, I had no credit. Well, actually I did, and it was bad. But I found a mortgage broker who’d loan me money based on the equity in the property, not my credit. His name was Al, and he would loan me 60% of its value. Therefore, my credit was irrelevant. His sole interest was the collateral, not my credit. Sure, the interest was high, but the money was easy to get. No application. No committee approval. No long wait. The loans closed two days after I got an appraisal and…

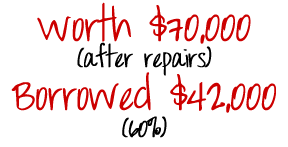

If the house was worth $70,000 after repairs, I knew I could borrow $42,000 (60%), so all I had to do was buy it cheap enough to make sure the loan would cover all my costs and then some. In addition to the 18% interest, I was paying Al ten points, that’s 10% of each loan as a broker fee. After I did a few loans, I learned it wasn’t even Al’s money I was borrowing.

If the house was worth $70,000 after repairs, I knew I could borrow $42,000 (60%), so all I had to do was buy it cheap enough to make sure the loan would cover all my costs and then some. In addition to the 18% interest, I was paying Al ten points, that’s 10% of each loan as a broker fee. After I did a few loans, I learned it wasn’t even Al’s money I was borrowing.

![]()

It wasn’t institutional money. No banks were allowed. It was money from Al’s friends, relatives and business associates. Just plain ole people who wanted to get a high rate of return on their money. And you gotta admit, 18% certainly qualified. But that’s not all. Every time I paid one of those loans off, I had to pay the lender six months’ extra interest. That’s called a prepayment penalty. What an ugly price to pay for money, right? I sure thought so, and that’s why I only borrowed from Al 76 times before I quit.

It didn’t take me long to figure out it wasn’t the cost of money that’s important, but the availability of it. Without Al’s money, I couldn’t pay cash for houses and, thereby, get them dirt cheap. With Al’s money, I could buy fast and get them fixed and sold quickly. You see, every time I paid ole Al 18% and 10 points…

He got his profit and broker fee, the lender got a high return, and I got easy money. A couple of years later, I started asking for money from people I knew and discovered it was easy to get. Very quickly, I had more money available than I could use, and I got better terms when I eliminated Al.

He got his profit and broker fee, the lender got a high return, and I got easy money. A couple of years later, I started asking for money from people I knew and discovered it was easy to get. Very quickly, I had more money available than I could use, and I got better terms when I eliminated Al.

I started paying 15% interest, three months prepayment penalty and eliminated the 10% brokerage because Al wasn’t the middle man. Then, a couple years later, I got a mortgage broker’s license and started loaning other people’s money to my real estate investor friends. Of course, I got paid a fee.

I Was Now Collecting The Same 10% I Used To Pay Al

But this letter is not about being a mortgage broker. It’s about finding all the money you need for your deals, so you can take advantage of the biggest foreclosure bonanza of our lifetime. It’s also about eliminating Al, so the money you find has no middle man making the rules. You make your own rules.

FYI, today, I borrow money from ordinary people just like I did back then, except the interest rate is 7% and no points are added.

I don’t make monthly payments. That’s right. The interest accrues, so I have no mortgage payments to make. Imagine what that will do to your cash flow while awaiting a buyer for your house or after you install a lease option tenant and start collecting rent with no payments.

![]()

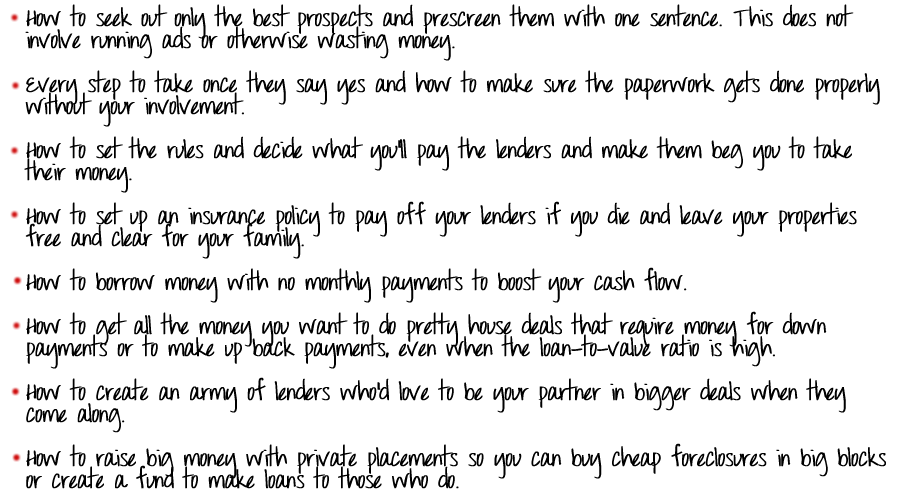

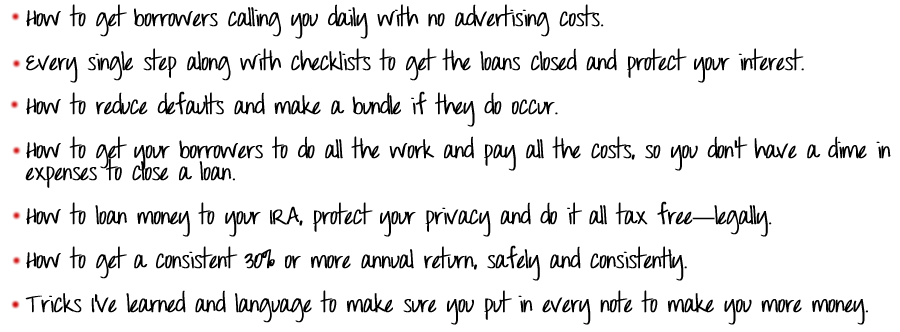

I decided to teach everything I know about private lending to all my students who want to learn. So, I held a 2-day boot camp called …The Private Lending Boot Camp. I recorded the boot camp and now my Private Lending Home Study Course is available for you

It has one purpose: To help you find all the private lenders you need to fund your own deals.

![]()

Hey, if you’re gonna make friends, you might as well make friends with people who ain’t broke.

![]()

Well, now you can be. Just like the banks do. Loan out your money, and get paid well. On the Private Lending Boot Camp Home Study recordings, you’ll learn…

I’ll also share with you all the mistakes I’ve made over the last 24 years as a mortgage broker and save you a lot of grief. Man, these seminars in the School of Hard Knocks are expensive.

IRAs and pension plans are a great source of funds if you know how to tap into them and who to ask. I’ll show you. Actually, there isn’t much you’d want to know about finding and brokering private money that I don’t cover in this course. You’ll be participating in asking for money, answering objections and closing deals.

The recordings come with a complete systems manual. It’s a masterpiece that has been two years in the making. It’s got everything you need to find money and become a private lender.

Look, if you’re gonna buy and sell houses, these boot camp recordings are an absolute must. Raising money is an important ingredient, especially if you intend to buy junkers. You can also get through life without eating foods that taste good and running ten miles a day. But why?

The retail cost of these recordings is $1,997, but I’m giving it away for only $997! That’s a $1,000 discount. The fee is minimal, but the long-lasting effects of this boot camp will serve you for life.

To Your $uccess,

Ron LeGrand

Millionaire Maker

Reviews

There are no reviews yet.